Decoding Fintech Lending

While the fintech lending sector started in 2013-2014 with focus on SME lending, it slowly added personal loans & purchase financing in 2014-15. Off late, there have been specialist startups focusing on supply chain, education & training, travel, health, P2P lending etc. And to support this growth, lending start-ups have been garnering the most capital from investors across the Fintech landscape.

The Indian FinTech Landscape has been through a sea change in the last 5-6 years. Lending has been one of the primary offerings that start-ups in this sector have been vying for. We have observed great progress in this segment from the earlier ‘paper & process’ heavy interactions to the current lending within a few seconds. There have also been a few learnings along the way.

Let us take a look at their business models and what the future holds for FinTech lending in the fast-growing Indian market.

There is diverse range of Lending Products that are available in the Indian market. While the fintech lending sector started in 2013-2014 with focus on SME lending, it slowly added personal loans & purchase financing in 2014-15. Off late, there have been specialist startups focusing on supply chain, education & training, travel, health, P2P lending etc. And to support this growth, lending start-ups have been garnering the most capital from investors across the Fintech landscape. A few large & growing startups in this segment include Capital Float, LendingKart, Neogrowth, Indifi, Kissht, EarlySalary, Krazybee, Zest Money, Moneytap, Paysense etc.

While some start-ups act as intermediaries / market places, many are eventually setting up their own NBFCs and starting to lend from their own funds.

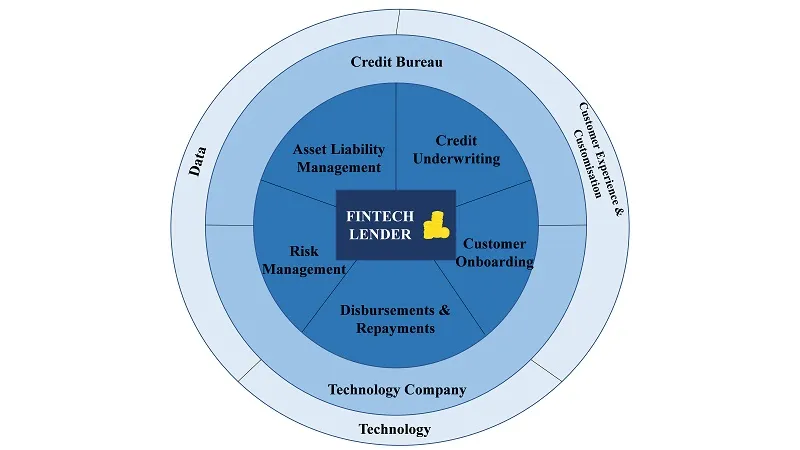

A careful analysis of these business models shows 3 key components:

Outer Cover:

Fintech Lenders use data and technology innovations to provide superior customer experience and a wide range of customizations. This was hitherto not feasible for the large legacy lenders. While traditional lenders have started using technology significantly, they are still not at par to compete with the startups in their innovations, nimbleness and new customer & segment identification. Key innovations by the fintech lenders have been across digital sourcing, use of alternate data, processing & disbursement lead times, risk analytics, etc. While they are competing with the traditional lenders, they are also expanding the market for lending as a whole by bringing in more ‘new to credit’ borrowers.

Inner Layer:

To perform the above activities, Fintech Lenders need to simultaneously play the role of a technology company and a credit bureau. They are extremely digitally savvy (similar to e-commerce companies) in obtaining and using data to source / underwrite/manage risk / develop products etc. Given the lack of established bureaus of alternate data for borrowers without a formal credit history, they wear the hat of a credit bureau too. Loans are being extended to ‘new to credit’ borrowers based on parameters including SMS history, social media behavior, etc.

The Core:

All the above features have resulted in Fintech Lenders behaving and being perceived a lot like new-age digital startups than erstwhile lenders. They are willing to spend big marketing bucks while also experimenting with new data sources.

However, at the heart of it, the business model requires the fundamentals of a lending company – underwriting, KYC, collections, asset-liability management, and leverage. A successful lending business will be set up only when the fintech does not lose focus of the fundamentals - any company can lend large sums of money, but managing collections will differentiate ‘good one’ from the ‘also ran’.

And these fundamentals are what are being tested over the past 1 year. The debt market in India is reeling post the ILFS, DHFL, and other debacles. Funding sources have tightened for lenders with banks, MFs, NBFCs becoming more stringent. To add to these funding challenges, there are process challenges in the form of Aadhaar / eKYC restrictions (impacting KYC and onboarding of borrowers) and restrictions by Android Playstore on reading text messages and other data on phones (impacting the availability of alternate data).

However, not everything is gloomy for them. EY Global FinTech Adoption Index 2019 rates India as the joint leader globally with an adoption rate of 87% for consumer fintech products. RBI has started working on sandboxing which enables FinTechs to quickly test and scale innovations. Large Banks and Financial institutions too have realized the importance of taking the digital route and have started partnering with FinTech firms to cater to new markets (co-lending arrangements, accessing alternate credit data, etc).

The huge Indian population with more than half of the addressable population still to be tapped for financial services inclusion makes the FinTech lenders essentials to the system. Besides, more and more 'new to credit' borrowers are getting a credit history, so fintech lenders can be the stepping stone for their longer-term credit access.

With this current mix of headwinds and tailwinds, this sector is going through a testing phase and this ‘downtime’ in business needs to be traversed intelligently. Fintech lenders would do good to themselves by using funds intelligently, improving algorithms, managing cashflows, treading cautiously in new areas & customer segments and building robust processes before scaling up.

We have seen the first enthusiastic wave of fintech lending with many start-ups joining the bandwagon. However, with the harsh reality set in, the good ventures will gradually be separated from the not-so-good ones. Some would shut shop, some merge into larger entities and some would be acquired (by traditional lenders too for their tech platforms?).

Going forward, the second wave will start where those who have proven their mettle, will compete to scale significantly. We will see more partnerships between banks / NBFCs and Fintech lenders to start reaching out to the untapped segments and offering new products.

And that would give us the 1st fintech lending unicorn of India.